US Income Taxes

Introduction to US Taxes

US Income Tax Basics

All international students, scholars, and employees have US income tax obligations. Knowing and following these tax obligations is essential to maintaining valid immigration status.

Income tax issues come up at two primary times:

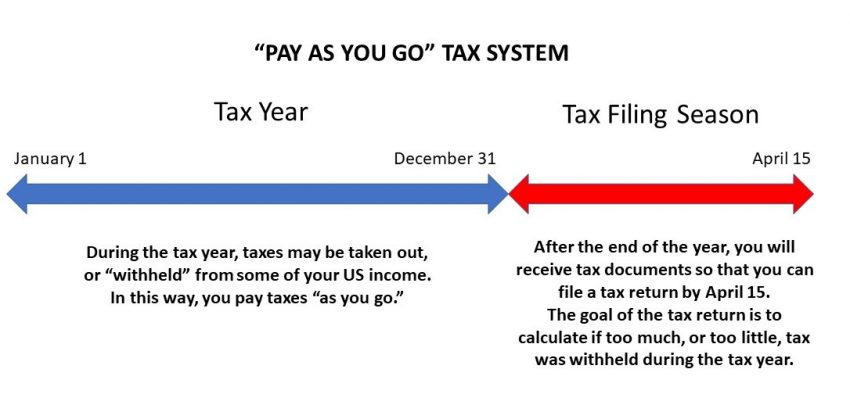

- When starting a job, or when receiving other taxable US income such as a taxable stipend (tax withholding). The US has a "pay-as-you go" tax system (see below), which means that income taxes can be withheld from you part when you start a job (or when receive other types of taxable income, such as a taxable scholarship or fellowship). In these situations, your employer or income provider may be required to withhold some of your income as taxes. See the information below about the "pay as you go" tax system. You may need to complete a Foreign Tax Analysis as well as other paperwork that determines how much taxes are withheld from your pay or stipend.

- During the annual tax filing season (tax return filing). By April of every year, you may need to file a tax return or other tax form to report your tax situation for the previous tax year. For example, the tax year January 1 - December 31, 2025, the tax filing season starts in January of 2026 with a tax filing deadline of April 15. During the tax filing, you will report how much income you earned during the tax year, how much in tax was already withheld, and calculate whether you have a tax bill (you owe more tax) or can get a tax refund (you paid more tax than you owe).

- Additionally, nonresidents who were present in the US any days during a calendar year should still plan to file a tax return for that year, even if they earned no US-sourced income for that year! While you will not owe taxes or be due a refund, you should still file Form 8843. Please see our "No Income" page details on the tax filing process for those who did not earn US-sourced income in a given year.